29 / 231

29 / 231

Brasil

PackTrends

2020

29

packaging market: world and Brazil

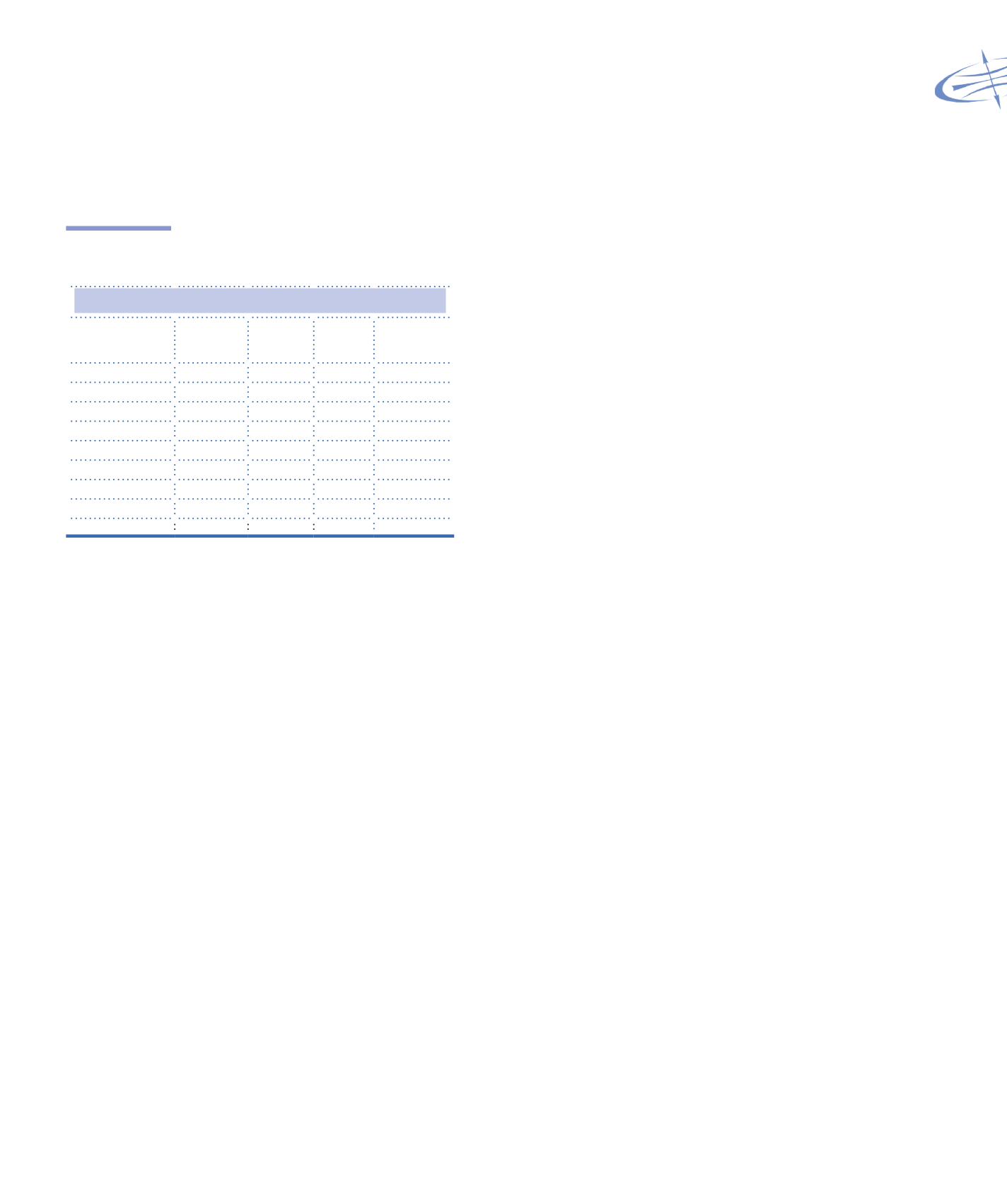

Table 1.47

Beverages industry: principal

products by sales (2008-2011)

Principal products by sales (R$ Billion)

2008

2009

2010

Average

growth

(2008-2011)

Beer

44

46

52

4.1%

Soft drinks

27

28

27

0.7%

Milk

24

27

26

1.8%

Spirits

10

10

11

2.9%

Fruit juices

10

11

12

7.6%

Coffee & Tea

10

11

11

1.4%

Other beverages*

5

6

6

6.6%

Tonic drinks**

2

3

3

14.1%

TOTAL

132.7

141.2 149.8

3.3%

*It includes mineral water and RTD tea

**It includes isotonics, fermented milk, energy drinks and nutritional

supplements.

Source: DATAMARK

Higher purchasing power allows the Brazilian

consumer to try new products, a trend that leads to

important changes in consumer habits. The premium

beer segment has, nowadays, 7% of the beer market.

In the last 5 years,, that segment has grown at a 10%

average rate a year, a higher rate than the 4.1% for

the total beer market. The sales of Stella Artois beer,

Ambev’s premium brand, for example, had a 215%

increase in sales in 2011 (FACCHINI, 2012).

There is a growing demand for products with a new

offering in the juice market as well. Many companies,

such as Juxx, Danone (with the brand Activia) and

Globalbev (with the brand Amazoo), among others, have

launched juices with unusual flavors, like cranberry,

with functional ingredients and no preservatives.

The Federal government readjusted IPI, PIS and

Cofins tax rate table in June 2012 for the cold beverage

market – water, soft drinks, beer, isotonics and energy

drinks, increasing the tax burden for the sector by 19%

on average. However, in September the Federal Tax

Authority delayed the tax increase, which should have

come into force in October, through to April 2013. In

exchange for the delay, the beverage producers promised

to keep up investments and employment. However, the

sector will pay more taxes due to increases over the

last 12 months. That is because beverages are taxed a

fixed value per unit instead of a percentage of the price.

That fixed value is updated every year and this year,

the likely increase to the final consumer may be up to

2.15%. Thus just as in 2011, it is possible that the

increase in the shelf prices might reduce consumption

(FERNANDES; VERÍSSIMO, 2012).

The higher purchasing power of the emerging

middle class has directly contributed for a higher

demand for aluminum canned beverages, mainly beer.

Between 2007 and 2011, the volume of aluminum cans

used to package beer increased 56%, from 7.8 million

to 12.2 million of units, increasing their share of the

market from 28% to 34% in the period (DATAMARK,

s.d.). The increase of the Brazilian consumer’s

discretionary income has enabled a change in their

purchasing behavior that encouraged beer consumption

at home, an occasion where aluminum cans are more

appropriate compared to returnable glass bottles. Other

markets that have pushed up the demand for aluminum

cans are juices, energy drinks and RTD tea.

The advancement in the ecofriendly packaging

accompanies the endless search for cost reduction of

PET bottles by brand owners. Since they started to be

used in the soft drinks market, PET packages have had

cost reductions between 8% and 26%, depending on

size through light-weighting both in the neck and bottle

cap. Besides reduced consumption of raw material,

another important trend in the PET bottle transformation

process, influenced by sustainability issues, is the use

of resin from renewable sources that accounts for up

to 30% in bottles used in the soft drinks and mineral

water markets (PACHIONE, 2010).

The huge dependency on PET bottles in the

soft drinks market (approximately 60%) has forced

the material converters to seek new opportunities to

replicate the success of PET bottles in other promising

markets. The Portuguese company Logoplaste, along

with the brand Shefa, for example, seems to have

started a migration from the aseptic cartons to PET

bottles with light barrier in the UHT milk market. In only

6 months, Shefa has packed 30% of their production in