28 / 231

28 / 231

Brasil

PackTrends

2020

28

packaging market: world and Brazil

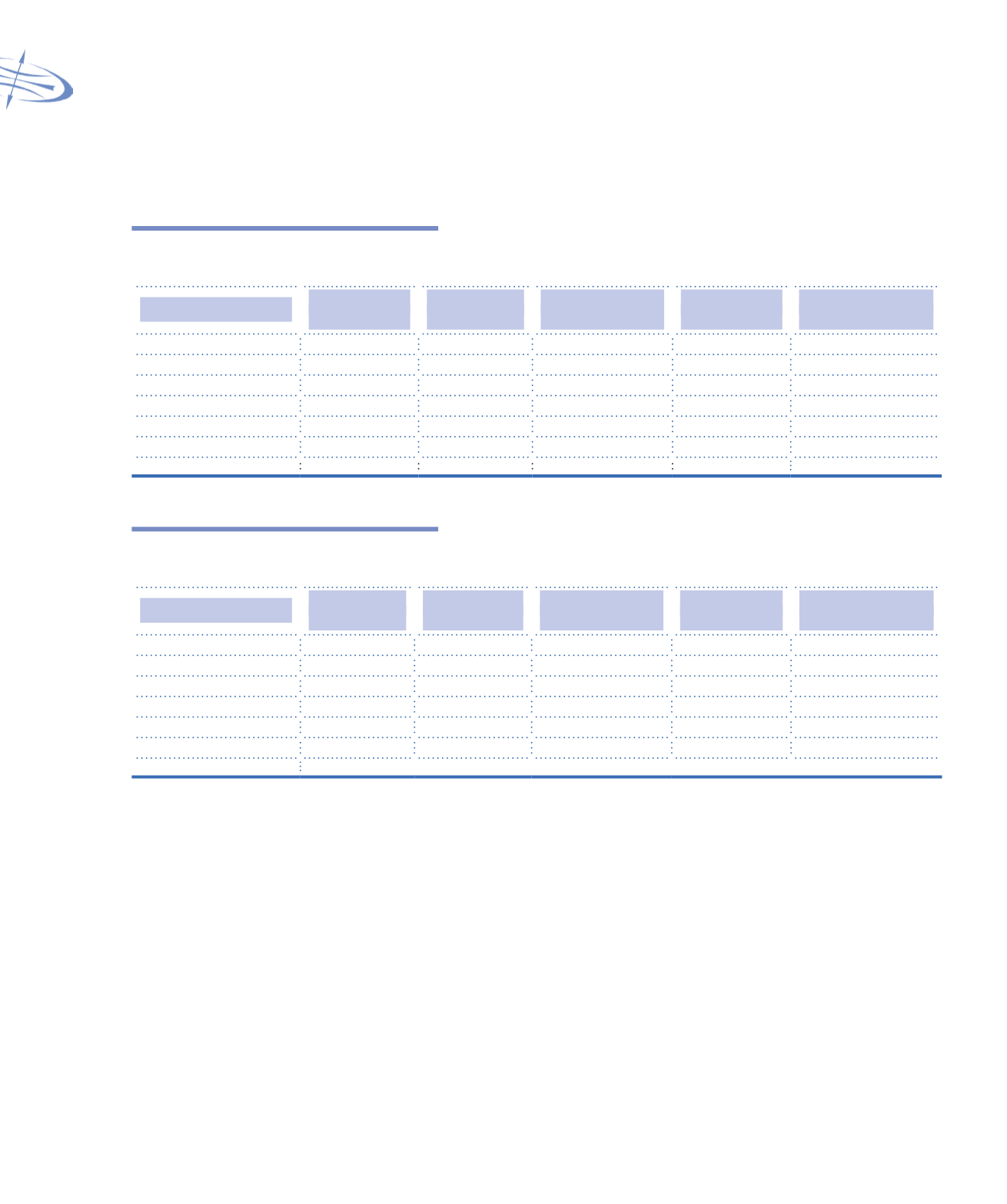

Table 1.45

Historical trends and projections for food packaging consumption:

Volume (units)

Material

Billion units

2007

Billion units

2011

Average growth

2007-2011

Billion units

2015*

Average growth

2011-2015*

Corrugated board

6.2

7.0

3.4%

8.6

5.2%

Plastics

83.7

94.8

3.2%

107.3

3.1%

Metals

8.3

8.0

-0.8%

9.7

5.0%

Paper and board

14.0

16.5

4.2%

18.5

2.9%

Glass

1.2

1.1

-1.4%

1.2

3.1%

Flexibles

94.1

103.6

2.4%

115.9

2.9%

TOTAL

207.4

230.9

2.7%

261.2

3.1%

*Estimate

Source: DATAMARK

Table 1.46

Historical trends and projections for food packaging consumption:

Volume (tonnes)

Material

Billion units

2007

Billion units

2011

Average growth

2007-2011

Billions units

2015*

Average growth

2011-2015*

Corrugated board

1,229.0

1,415.2

3.6%

1,666.2

4.2%

Plastics

558.0

633.3

3.2%

769.5

5.0%

Metals

432.8

390.9

-2.5%

478.9

5.2%

Paper and board

312.0

359.8

3.6%

404.0

2.9%

Glass

189.2

170.3

-2.6%

190.1

2.8%

Flexibles

142.0

155.4

2.3%

179.8

3.7%

TOTAL

2,863.0

3,124.9

2.2%

3,688.9

4.2%

*Estimate

Source: DATAMARK

Beverage industry sales in Brazil reached R$ 151

billion in 2011, an advance of less than 0.9% in relation

to the previous year, way below the growth registered

in 2010 (6.1%). The low growth was due to the poor

performance of the beer segment which retracted

in 2011. One of the factors was an increase in PIS/

Cofins and IPI taxes, by about 15%, over beverages,

that resulted in a price increase of 1.3%. The higher

tax burden had an impact on the sector, especially on

brands with lower market shares. However, some sectors

maintained the good sales performance of previous

years, such as tonic drinks, pulled up by energy drinks

(33%) and isotonics (30%), and fruit juices (15%).

Table 1.47 shows the main products in this segment,

by sales, for the period of 2008-2011.

User industry: beverages