27 / 231

27 / 231

Brasil

PackTrends

2020

27

packaging market: world and Brazil

One of the main factors responsible for the

continuous growth of the sector, the accelerated

economic development of the country in the later years

has brought to the market a new emerging middle class

with a higher purchasing power and a more demanding

level of quality for basic food products. These changes in

the purchasing behavior have intensified rivalry among

the industrial food producers, which seek to attract

new consumers with innovative products packed in

attractive and functional packaging. In 2010, there were

105,589 launches of new food products, an increase

of 4.3% comparing to 2009, however, the demand for

healthy, light, fresh, natural and organic food, as well as

functional and fortified options, must continue to grow

in the coming years. The sales channels have suffered

significant changes, with convenience stores becoming

more important points of sales for consumers of all ages

and origins (THE FUTURE... 2009).

Characteristics such as lightness, safety and

transparency are also more highly valued by consumers.

As a result, flexible packaging consumption has been

stimulated by perishable and convenience foods, thanks

to the growth and regularization of cheese, meat and

cold cuts market. Investments in new packaging have

been an efficient form for the brand owners to strengthen

their brands and differentiate themselves from their

competitors. In some markets, these innovations have

catalyzed significant changes in the packaging mix,

such as in the tomato sauces segment, which replaced

tinplate cans with stand-up pouches.

The food segment will increase packaging

consumption, with average rates of 4.4% a year, in value

(US$ millions), and 4.2% in volume (tonnes), between

2011 and 2015. Metal and plastic packaging should

show the highest growth rates (

Tables 1.44, 1.45 and

1.46

).

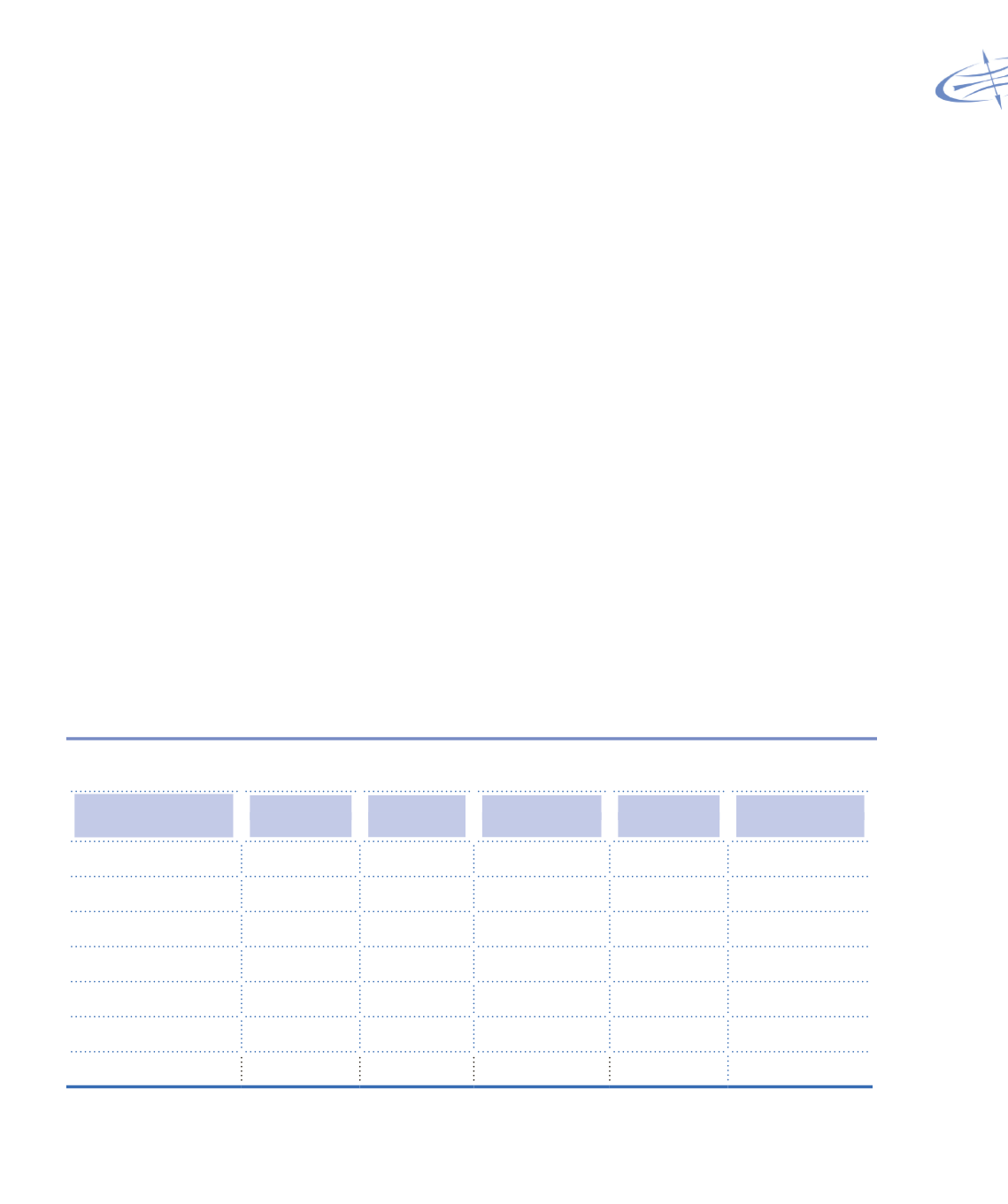

Table 1.44

Historical trends and projections for packaging consumption for food: Value

Material

US$ million

2007

US$ million

2011

Average growth

2007-2011

US$ million

2015*

Average growth

2011-2015

Flexibles

3,402

4,196

5.4%

4,856

3.7%

Plastics

2,422

3,235

7.3%

3,932

5.0%

Paper and Board

1,917

2,584

7.7%

3,054

4.3%

Corrugated board

1,557

1,844

4.3%

2,171

4.2%

Metals

1,212

1,613

7.4%

1,976

5.2%

Glass

174

192

2.5%

215

2.8%

TOTAL

10,705

13,665

6.3%

16,204

4.4%

*Estimate

Source: DATAMARK