14 / 231

14 / 231

Brasil

PackTrends

2020

14

packaging market: world and Brazil

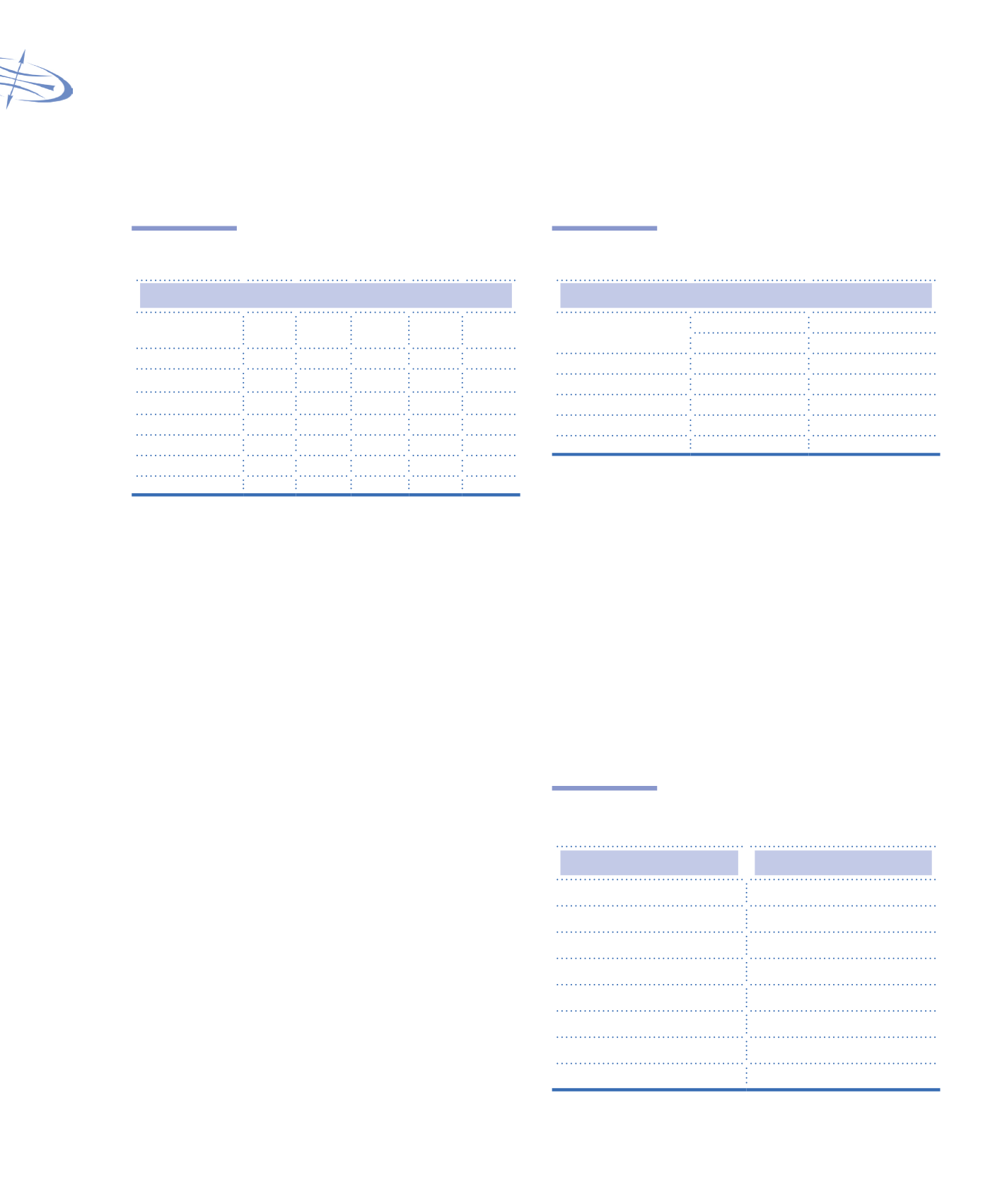

Table 1.5

Industrial segment shares: Plastics,

Cellulose, Metals, Glass and Others

Global share in value by material (US$ billion)

Material

2010

Value

Share

%

2015

Value*

Share

% CAGR

Paper & board 209 31% 254 30% 3.2%

Plastics

142 21% 203 24% 6.2%

Flexibles

128 19% 169 20% 4.7%

Metals

101 15% 118 14% 2.6%

Glass

47 7% 51 6% 1.2%

Other

41 6% 42% 5% 0.7%

TOTAL

675

845

3.8%

*Estimate

CAGR: Compound Annual Growth Rate

Source: MARKET..., 2008

Table 1.6

Share of industrial segments:

Brazil x World

Share - Value (US$)

Material

BRAZIL%

GLOBAL %*

2009

2009

Paper & board

26%

32%

Plastics

27%

23%

Flexibles

22%

20%

Metals

19%

16%

Glass

6%

8%

*Adjusted percentages

Source: DATAMARK

1.2 PACKAGING SECTOR IN BRAZIL

Industrial companies

Table 1.8 shows the largest packaging companies

in the world and identifies those with operations in

Brazil. In the country (

Table 1.9

), note that seven out of

ten of the largest companies are Brazilian.

Table 1.7

Number of companies and share in

the total industry – Brazil

Operation

Number of companies

Rigid plastics

220

Flexibles

200

Plastic films

180

Paperboard

70

Corrugated board

60

Metal packaging

38

Caps

12

Aseptic cartons

2

Source: DATAMARK

The data available from trade associations and

other recognized organizations shows 782 companies

in the packaging sector working in Brazil. The sample

covers, approximately, 70% of the market, includes

registered companies (

Table 1.7

). The majority are

companies in the plastics segment.

Datamark’s classification for the companies

shown in Table 1.7 is:

• Rigid plastics:

converters of blown and/or injected rigid

plastic packaging.

• Flexibles:

converters of laminated and/or co-extruded

packaging.

• Plastic films:

converters of monolayer plastic

films (more “commoditized” products with less

differentiation)

• Paperboard:

Includes integrated converters of cartons

and other paperboard packaging and also the

principal printing companies.

• Corrugated board:

manufacturers of corrugated board

packaging/sheet (includes ABPO associates and an

estimate of non-associated players).